Outsiders usually have difficulty distinguishing a broker from a market maker, and this time it’s no different. Strange thing is even Euronext is confused. Every firm is a trading firm. Wouldn’t surprise me if some people at Euronext have the title “trader” on their business cards themselves.

Outsiders usually have difficulty distinguishing a broker from a market maker, and this time it’s no different. Strange thing is even Euronext is confused. Every firm is a trading firm. Wouldn’t surprise me if some people at Euronext have the title “trader” on their business cards themselves.

Anyway, the trading floor at the exchange building was deserted after All Options retreated to its headquarter at the Herengracht. No financial worries for Euronext, as All Options has a contract to pay 50k monthly until december 2012, but it doesn’t give the same important feeling : hitting the opening bell above an empty office.

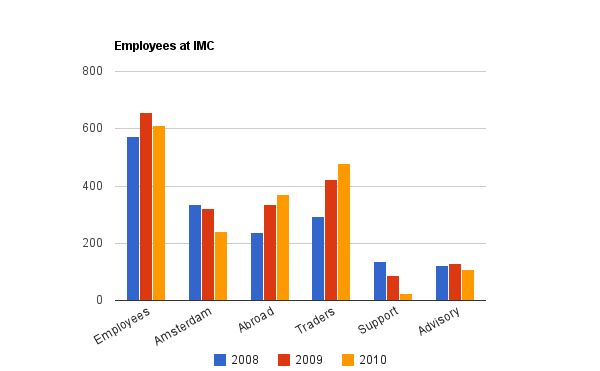

As Scrocca and Flow Traders are perfectly happy at their current – somewhat remote – locations, the trading floor will be split up between four firms. Building large walls would harm the atmosphere, so walls of glass will provide the privacy between the new renters. Not only for privacy, it will also function as Chinese walls. The regulatory watchdog won’t permit proprietary traders setting next to wholesale brokers. Euronext is explicitly speaking of 100 traders to fill the trading floor. Sold. Anyway, the new tenants are:

- Leopark. A small option market maker consisting of old school traders from the open outcry era. Trading some minor option classes such as Wereldhave, but have a good reputation in the AEX index options. Moving in from another small office inside the exchange building.

- AFS. A broker. Earning a fee when executing large blocks of options between financial institutions. Doing trades with market makers, but never taking on a position (unless by accident). Their head of research and news, Jacob Jurg, has been awarded awarded the nr. 1 analyst ranking in the 2011 Thomson Reuters Extel Awards; Derivatives Trading/Execution.

- Nyenburgh. Trading in the delta one spectrum. Daytrading and ETF arbitrage, although moving at a slower pace than Flow Traders – it competes successful as a small firm against much bigger rivals in the ETF space.

- Mijnbroker.nl. A new contender for Binck, a retail broker with apparently competitive rates.

The press release also states “Criterion Arbitrage & Trading” will be renting another trading floor. Never heard from them, and neither does google. But it turns out to be the new company from Gert de Rover – a well respected and former director at All Options. They will occupy the Obligatiezaal.

Other news (Optiver, Goldman Sachs)

Last week the class action against Optiver and the alleged oil manipulation scheme was stayed, again. The CFTC is pushing for a mediated settlement with Optiver. This civil lawsuit drags on for three years now.

Another interesting story on the mispricing of warrants in Hong Kong has been published somewhere else. Goldman introduced warrants and initially mistakenly priced them 100 fold too low. Thanks to a commenter we have a perfect summary of the story.

“On March 31 warrants linked to Japan’s Nikkei 225 index and sold by GS began to spike in value, because, it now seems likely, a single investor had noticed what proved to be a small but serious error in the settlement documents. Rather than settle at closing level minus strike level times index currency amount divided by exchange rate, the original documentation multiplied by the prevailing exchange rate. The substitution of a multiple sign meant in theory that the warrants were worth more than 100 times their intended value.

On April 21, GS announced that it would buy back the warrants at 110% of the higher of the price paid or the total buyback value of the warrants, plus an admin fee of HK$5,000 ($643).

In a letter seen by Euromoney, one investor claims to have lost time value while the warrants were suspended, that it is unreasonable that GS be able to dictate the terms of the settlement without negotiation; and that both the HKSE and the regulator have ducked responsibility and left the product issuer to decide how to proceed.“

Here’s a full copy of the original text in Euromoney on the warrant fiasco – kudo’s to commenter who scanned the piece.

For sale on eBay, an original Van der Moolen statue depicting the classic fight between bull and bear, with a very catchy slogan “the legend lives on“. Guess the old Van der Moolen himself could never have imagined to live on in secondhand markets.

For sale on eBay, an original Van der Moolen statue depicting the classic fight between bull and bear, with a very catchy slogan “the legend lives on“. Guess the old Van der Moolen himself could never have imagined to live on in secondhand markets.

{kind=link}