Record year for IMC

It’s a common habit for trading firms to postpone the release of financial results as long as is legally possible. Last february IMC released the results over 2009 – and all of a sudden Pot and Defares decide to share the information on 2010 results with the rest of the world. If intended to surprise this website, they have succeeded. Didn’t see this one coming – although the great results didn’t really come as a surprise. The rumor of a record year in terms of profits has proven correct. IMC net profits rose 96% to 51 million (2009: 26 mio). Quote reports half of the 51 million net profit is paid out as dividend, flowing in the pockets of shareholders Wiet Pot (9 mio) and Rob Defares (15,5 mio).

It’s a common habit for trading firms to postpone the release of financial results as long as is legally possible. Last february IMC released the results over 2009 – and all of a sudden Pot and Defares decide to share the information on 2010 results with the rest of the world. If intended to surprise this website, they have succeeded. Didn’t see this one coming – although the great results didn’t really come as a surprise. The rumor of a record year in terms of profits has proven correct. IMC net profits rose 96% to 51 million (2009: 26 mio). Quote reports half of the 51 million net profit is paid out as dividend, flowing in the pockets of shareholders Wiet Pot (9 mio) and Rob Defares (15,5 mio).

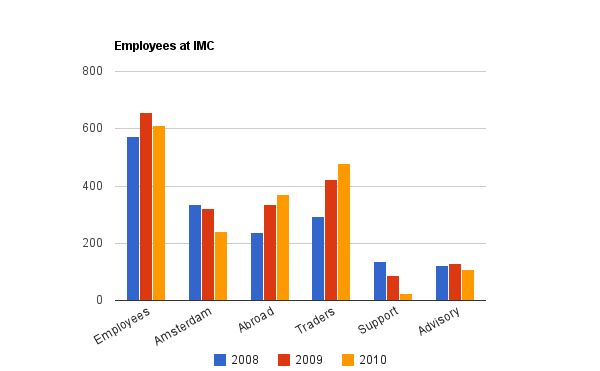

This year it’s fairly easy to see where the profits are coming from. The traders earned 61 million more than 2009, the net trading result in 2010 was 273 million. On average they earn a million a day, that’s pretty decent. A higher trading result usually means higher bonuses for the traders. The average salary and bonus per employee was 228.000, which is exactly 50% higher than 2009 (152k). The average headcount for 2010 was 613 (2009: 657) and they continue with the trend to hire people abroad and fire staff in Amsterdam. Frankly, this is an understatement as the Amsterdam office got rid of 81 people, from 322 down to 241. Mostly support staff probably, and management was smart enough to keep the best football players within the company. Cutting some overhead staff is fine, but somehow it’s hard to imagine running offices in half a dozen countries with only 25 support staff. The developers are probably being rebranded as “trader” or “advisor”.

Have a look at the financial statements in this searchable pdf and for triumphant annual report see here. Key message in the last one is they made a successful shift in more automated trading, away from the good old manual market making.

{kind=link}

Why do they need so many advisory staff? What are the advice staff anyway – are they developers/ management HR?

Advisory staff is from Cardano (consultancy) and IMC Asset Management

that seems to be a huge amount of traders, over 75% of all staff from the looks of those charts. hard to believe its actually that high

I think the term ‘trader’ is being used pretty loosely here….

who cares ?

not so long ago a lot of comment was about how badly IMC is. Now,look at the figures.

Fancy annual report all of a sudden, fast publication; Goldman Sachs’ like business principles ? My bet they are trying to go public second half of the year ! Looking for the 9 digit market cap.

look wat happened to VDM .. its better kept private ..

I think you mean ten digit market cap. The net asset value of the company is probably nine digits.

Yes, I meant 10 digit, you are right; I guess I confused what I think it’s worth, and what they think it’s worth

If a trader doesnt need the access to extra capital, and is selling shares in his trading company, would you buy it ?

If it’s in All Options then I would buy for sure!

anonymous

June 21st, 2011 at 12:31 pm

If a trader doesnt need the access to extra capital, and is selling shares in his trading company, would you buy it ?

—

Wiet Pot did. He bought 35% in IMC. Already got 14 mio dividend (at least) and guess the share price has risen considerably since 2008..

i was talking in terms of outside investor .. not as wein pot who is now involved in running the company ..

is eclipse option a good place to work? is it true there is not much bonus for the staff

thats true for most places .. money is retained mostly by partners, get real, you are easily replacable, unless of course you are a star, in which case you’ll be made partner and you can enjoy the riches you actually deserve ..

Impressive, most impressive.

New York (June 22, 2011) — A New York federal judge on Wednesday stayed three consolidated investor class actions accusing Optiver Holding BV of manipulating crude oil prices as the U.S. Commodity Futures Trading Commission pushes for a mediated settlement with the Dutch trading company.

U.S. District Judge Loretta A. Preska stayed the civil cases after referring the CFTC matter to mediation for a possible settlement on June 15. No time frame for the mediation was available, and neither the defendant nor the CFTC immediately returned requests for comment Wednesday.

Some states set a 30-day limit on mediation. I don’t know if this applies to New York.

More stalling techniques. Seems they just want to keep kicking the ball down the road until the US forgets about it.

rtl-z is ook wakker geworden:

http://www.rtl.nl/%28/financien/rtlz/print/%29/components/financien/rtlz/2008/weken_2008/30/0725_0915_optiver_oliecontracten.xml

‘More stalling techniques. Seems they just want to keep kicking the ball down the road until the US forgets about it.’

of course with time, interest to hurt offender goes down, but also the PV of the fine goes down as the fine reserves are earning returns .. 50 million fine earns 2million@4% returns every year ..

I’ll email the CFTC lawyers with that just to make sure.

@5.57pm – wow you are real genius…. you think optiver pays their lawyers less than 2million per year?

asshole

@9:22am – you think optiver have actually seen the inside of a courtroom?

jackass

‘you think optiver pays their lawyers less than 2million per year?’

how much is the legal fees annually ?

http://www.euromoney.com/Article/2841062/Category/19/ChannelPage/169/Goldmans-warrants-fiasco-is-a-bad-sign-for-HK-structured-products.html

i’ll post the summary of the article in a bit ..

On March 31 warrants linked to Japan’s Nikkei 225 index and sold by GS began to spike in value, because, it now seems likely, a single investor had noticed what proved to be a small but sureious error in the settlement documents. Rather than settle at closing level minus strike level times index currency amount divided by exchange rate, the original documentation multiplied by the prevailing exchange rate. The substituion of a multiple sign meant in theory that the warrants were worth more than 100 times their intended value

on April 21, GS announced that it would buy back the warrants at 110% of the higher of the price paid or the total buyback value of the warrants, plus an admin fee of HK$5,000 ($643)

In a letter seen by Euromoney, one investor claims to have lost time value while the warrants were suspended, that it is unreasonable that GS be able to dictate the terms of the settlement without negotiation; and that both the HKSE and the regulator have ducked responsibility and left the product issuer to decide how to proceed

The Dutch financial newspaper is reporting 2010 earnings of (net) 75 million for Optiver. So 2009 was the single year where IMC outperformed Optiver and now it’s back to normal.

http://www.glassdoor.com/Reviews/IMC-Financial-Markets-Reviews-E278100.htm

Recently on glassdoor.com there has been generally unfavorable reviews about IMC. Anyone know why?

I wouldn’t trust glass door so much mate. Optiver US has a bad report on that website but that doesn’t tell the whole story. Optiver US got rid of most management and is now finally running on all cylinders with proper structure on the trading and IT side of things. It took a while but everything is finally fixed at Optiver in the US.

Optiver US was plagued with shit traders to start with since early 2000’s who were paid for making no money. The resignation of three senior traders triggered the flushing down of all complacent mediocre personell down the toilet

Their immaturity to claim themselves as world travellers, explorers and professional on linkedin throws light on how bad they really were. Good luck finding a job elsewhere.

any update on IMC’s results. Looks like Optiver had a great 2011.